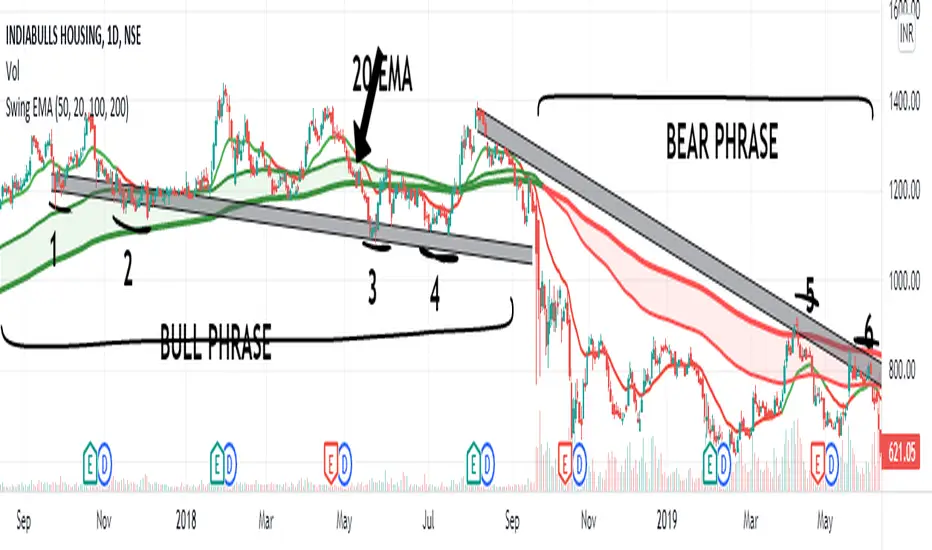

Swing EMAWhat is Swing EMA?

Swing EMA is an exponential moving average crossover-based indicator used for low-risk directional trading.

it's used for different types of Ema 20,50,100 and 200, 3 of them are plotted on chat 20,100,200.

100 and 200 Ema is used for showing support and resistance and it contains highlights area between them and its change color according to market crossover condition.

20 moving average is used for knowing Market Behaviour and changing its color according to crossover conditions of 50 and 20 Ema.

How does it work?

It contains 4 different types of moving averages 20,50,100, 200 out of 3 are plotted on the chart.

20 Ema is used for knowing current market behavior. Its changes its color based on the crossover of 50 Ema and 20 Ema, if 20 Ema is higher than 50 Ema then it changes its color to green, and its opposites are changed their color to red when 20 Ema is lower than 50 Ema.

100 and 200 Ema used as a support and resistance and is also contain highlighted areas between them its change their color based on the crossover if 100 Ema is higher than 200 Ema a then both of them are going to change color to Green and as an opposite, if 200 Ema is higher then 100 Ema is going to change its color to red.

So in simple word 100 and 200 Ema is used as support and resistance zone and 20 Ema is used to know current market behavior.

How to use it?

It is very easy to understand by looking at the example I gave where are the two different types of phrases. phrase bull phrase and bear phrase so 100 and 200 Ema is used as a support and resistance and to tell you which phrase is currently on the market on example there is a bull phrase on the left side and bear phrase on the right side by using your technical analysis you can find out a really good spot to buy your stocks on a bull phrase and too short on the bear phrase. 20 Ema is used as a knowing the current market behavior it doesn't make any difference on buying or selling as much as 100 Ema and 200 Ema.

Tips

Don't trade against the market.

Try trade on trending stocks rather than sideways stock.

The higher the area between 100 Ema and 200 Ema is the stronger the phrase.

Do Backtesting before real trading.

Enjoy Trading.

"moving average crossover" için komut dosyalarını ara

T3 crossover strategyHi everybody,

Hereby a simple strategy based on T3 moving average crossover. If people are interested we can also add some alerts in people are interested.

Phoenix085-Strategies==>MTF - Average True Range + MovAvgFIRSTLY, Here are a few who have influenced my pinescripting immensely recently:

@JustUncleL

@BigBitsIO

@TheArtofTrading

@QuantNomad

@SquigglesNiggles and many many many more.

Overview:

> This indicator is a simple crossover of Moving Averages.

> In addition I am using ATR rising as an indication for Trending Price.

> The entry is made once the smaller moving average crosses the bigger moving average, and also the Closes above the Smaller moving average.

> but the only twist here is,

- the ATR source is One timeframe Higher(In this case same as the session).whereas the source for the Moving averages is one Timeframe Lower.

>i.e., if the Session is 1D, the Indicator checks if the ATR is rising in the DAILY TIMEFRAME,

*_* the trade entry is made once the MOVING AVERAGE crossover happens on ONE TIME FRAME lower, as per example, ATR --> 1D = MA -->4H.

> Moving Average ->

- Thick -> Bigger MA,

- Thin and Transparent -> Smaller MA,

> Also, the Color of the Thicker MOVING AVERAGE Changes as Below:

- When LongCondition is satisfied --> Color=Lime

- When ShortCondition is satisfied --> Color=Red

- When neither condition is satisfied --> Color=Gray

NOTE:

1) There is a limitation in using the Securities function for FREE USERS --> Only 500 bars are allowed. So to use the indicators with more data, you need an upgraded TV account.

2) Strategy still needs Fine tuning, but for now, use the Thicker moving average color LIME FOR LONG ENTRIES and RED FOR SHORT ENTRIES.

This is Free for Use and share

powerful moving average crossoverThis script is a simplified version of John Ehlers's adaption of Dr. Kalman's optimum estimator as applied to price action (More can be found on this here: www.dimensionetrading.com). Here I have adapted two of these optimum estimators to work together to provide crossover signals. The user can choose the input of this filter in the 'input source'. The 'Ratio of Uncertainties' controls how adaptive the moving averages are, increasing this number will increase adaptivity and vice versa for decreasing. The 'Kalman Gain' allows the user to choose how much error to let into the calculation. The smaller this number is the quicker the moving average will approach price action.

In practice this indicator is much smoother than most other moving averages and has significantly less whiplash while still getting very early entries. If anyone wants to adapt this script for their own uses please feel free. Message me what you make with it, I am very curious what this can do when in the right hands!

Happy trading!

Easy [CHE] Easy — Minimalist Pine Script for detecting EMA direction changes to define fixed price zones for simple support and resistance visualization, ideal for manual trading workflows.

Summary

This indicator's programming is kept minimalist and super simple, with core logic in under 20 lines for easy comprehension and modification. It creates fixed price zones based on divergences between a base exponential moving average and its smoother counterpart, helping traders spot potential consolidation or reversal areas without dynamic adjustments. By locking the zone at the high and low of the signal bar, it avoids over-expansion in volatile conditions, offering a stable reference line colored by price position relative to the zone. This approach differs from expanding channels by prioritizing simplicity and persistence until a new qualifying signal, reducing visual clutter while highlighting directional bias through midpoint coloring.

Motivation: Why this design?

Traders often face noisy signals from moving averages that flip frequently in sideways markets or lag during breakouts, leading to premature entries or missed opportunities. This indicator addresses that by focusing on confirmed direction shifts between the base and smoothed averages, then anchoring a non-expanding zone to capture the initial price range of the shift. The result is a cleaner tool for marking equilibrium levels, assuming price respects these bounds in ranging or mildly trending conditions.

What’s different vs. standard approaches?

- Reference baseline: Traditional moving average crossovers or simple channels that update every bar.

- Architecture differences:

- Zones are set only on new divergence signals and remain fixed until reset by a gap from the prior zone.

- No ongoing high-low expansion; relies on persistent variables to hold bounds across bars.

- Midpoint plotting with conditional coloring based on close position, plus a highlight for zone initiations.

- Practical effect: Charts show persistent horizontal references instead of drifting lines, making it easier to gauge if price is rejecting or embracing the zone—useful for avoiding false breaks in low-volatility setups.

How it works (technical)

The indicator first computes a base exponential moving average of closing prices over a user-defined length, then applies a second exponential moving average to smooth that base. It checks if both the base and smoothed values are increasing or decreasing compared to their prior values, indicating aligned direction. A signal triggers when this alignment breaks, marking a potential shift.

On a new signal, if the current bar's high and low fall outside any existing zone (or none exists), the zone bounds update to those extremes and persist via dedicated variables. The midpoint of these bounds becomes the primary plot line, colored green if below the close (bullish lean), red if above (bearish lean), or gray otherwise. A secondary thick line highlights the midpoint briefly when a zone first sets, aiding visual confirmation. No higher timeframe data or external fetches are used, so updates occur on each bar close without lookahead.

Parameter Guide

EMA Length — Sets the period for the base moving average; longer values smooth more, reducing signal frequency but increasing lag. Default: 50. Trade-offs/Tips: Shorter for faster response in intraday charts (risks noise); longer for daily trends (may miss early shifts).

Smoother Length — Defines the period for the secondary smoothing on the base average; higher values dampen minor wiggles for stabler direction checks. Default: 3. Trade-offs/Tips: Keep low (2–5) for sensitivity; increase to 7+ if zones trigger too often in choppy markets, at cost of delayed signals.

Reading & Interpretation

The main circle plot at the zone midpoint serves as a dynamic equilibrium line: green suggests price is above the zone (potential strength), red indicates below (potential weakness), and gray shows containment within bounds (neutral consolidation). A sudden thick foreground line at the midpoint flags a fresh zone start, prompting review of the prior bar's context. Absence of a plot means no active zone, implying reliance on price action alone until the next signal.

Practical Workflows & Combinations

- Trend following: Enter long on green midpoint after a higher low touches the zone lower bound, confirmed by structure like higher highs; filter shorts similarly on red with lower highs.

- Exits/Stops: Use the opposite zone bound as a conservative stop (e.g., below lower for longs); trail aggressively to midpoint on strong moves, tightening near gray neutrality.

- Multi-asset/Multi-TF: Defaults work across forex and stocks on 1H–Daily; for crypto volatility, shorten EMA Length to 20–30. Pair with volume oscillators for confirmation, avoiding isolated use.

Behavior, Constraints & Performance

- Repaint/confirmation: Plots update on bar close using historical closes, so confirmed signals hold; live bars may shift until close but without future references.

- security()/HTF: Not used, eliminating related repaint risks.

- Resources: Minimal overhead—no loops, arrays, or bar limits exceeded; suitable for real-time on any timeframe.

- Known limits: Fixed zones may lag in strong trends (price drifts away without reset); signals skip if no gap from prior zone, potentially missing clustered shifts. Assumes standard OHLC data; untested on non-equity assets.

Sensible Defaults & Quick Tuning

Start with EMA Length at 50 and Smoother Length at 3 for balanced daily charts. If signals fire too frequently (e.g., in ranges), extend EMA Length to 100 for fewer but stabler zones. For sluggish response in trends, drop Smoother Length to 2 and EMA Length to 30, monitoring for added noise. In high-vol setups, widen both to 75/5 to filter extremes, trading speed for reliability.

What this indicator is—and isn’t

This is a lightweight visualization layer for EMA-driven zones, aiding manual chart reading and basic signal spotting. It is not a standalone system, predictive model, or automated alert generator—integrate with broader analysis like market structure and risk rules. (Unknown/Optional: No built-in alerts or multi-timeframe scaling.)

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Relative StrengthDescription:

This indicator provides a simplified yet powerful method for measuring a stock's momentum based on its proximity to its recent high. It is a direct implementation of a trading concept discussed in a lecture from the New York Institute of Finance.

Core Concept

The underlying theory, supported by academic research, is that a stock making a new high is one of the most bullish signals possible. Such stocks have a statistical tendency to continue making new highs in the near term.

Instead of requiring complex relative strength calculations against a universe of stocks, this indicator uses a simple and elegant ratio to act as a proxy for momentum:

Indicator Value = Current Close / Highest High of Lookback Period

A value approaching 1.0 indicates the stock is strong and nearing a new high. A value at 1.0 means a new high has just been made.

How to Use This Indicator

The indicator consists of two primary components:

RS Line (Teal): The core momentum calculation (Close / High).

Signal MA (Orange): A moving average of the NHRS Line, which acts as the trigger for signals.

The signals are generated based on the crossover between these two lines:

BUY Signal: When the RS Line crosses ABOVE its moving average. This suggests that short-term momentum is accelerating and a new uptrend may be starting. The background will turn green.

SELL Signal: When the RS Line crosses BELOW its moving average. This indicates that momentum is fading and it may be prudent to exit the position to avoid a decline. The background will turn red.

Indicator Settings

You can customize the indicator to fit your trading style and the timeframe you are analyzing:

High Lookback Period: Choose the period for the "Highest High" calculation. Options range from 1 Month to 12 Months (52 weeks), allowing you to measure short-term or long-term strength.

Moving Average Length: Adjust the length of the signal line's moving average. The lecturer defaults to 26 weeks for a six-month view.

Moving Average Type: Select the type of moving average for the signal line (SMA, EMA, WMA, HMA).

Credits and Inspiration

Proper credit is essential. This script is a practical application of a concept that builds upon foundational academic work.

The core idea that a stock's proximity to its 52-week high is an investable anomaly was detailed in the 2004 Journal of Finance paper:

"The 52 Week High and Momentum Investing" by Thomas J. George and Chuan-Yang Hwang.

The lecturer's contribution, which this script implements, was to simplify this concept into an actionable trading tool by applying a moving average crossover to generate clear and objective buy and sell signals.

Disclaimer: This tool is for educational and informational purposes only. It is not financial advice. All trading involves risk, and you should always perform your own research and backtesting before making any trading decisions.

Uptrick: RSI Histogram

1. **Introduction to the RSI and Moving Averages**

2. **Detailed Breakdown of the Uptrick: RSI Histogram**

3. **Calculation and Formula**

4. **Visual Representation**

5. **Customization and User Settings**

6. **Trading Strategies and Applications**

7. **Risk Management**

8. **Case Studies and Examples**

9. **Comparison with Other Indicators**

10. **Advanced Usage and Tips**

---

## 1. Introduction to the RSI and Moving Averages

### **1.1 Relative Strength Index (RSI)**

The Relative Strength Index (RSI) is a momentum oscillator developed by J. Welles Wilder and introduced in his 1978 book "New Concepts in Technical Trading Systems." It is widely used in technical analysis to measure the speed and change of price movements.

**Purpose of RSI:**

- **Identify Overbought/Oversold Conditions:** RSI values range from 0 to 100. Traditionally, values above 70 are considered overbought, while values below 30 are considered oversold. These thresholds help traders identify potential reversal points in the market.

- **Trend Strength Measurement:** RSI also indicates the strength of a trend. High RSI values suggest strong bullish momentum, while low values indicate bearish momentum.

**Calculation of RSI:**

1. **Calculate the Average Gain and Loss:** Over a specified period (e.g., 14 days), calculate the average gain and loss.

2. **Compute the Relative Strength (RS):** RS is the ratio of average gain to average loss.

3. **RSI Formula:** RSI = 100 - (100 / (1 + RS))

### **1.2 Moving Averages (MA)**

Moving Averages are used to smooth out price data and identify trends by filtering out short-term fluctuations. Two common types are:

**Simple Moving Average (SMA):** The average of prices over a specified number of periods.

**Exponential Moving Average (EMA):** A type of moving average that gives more weight to recent prices, making it more responsive to recent price changes.

**Smoothed Moving Average (SMA):** Used to reduce the impact of volatility and provide a clearer view of the underlying trend. The RMA, or Running Moving Average, used in the USH script is similar to an EMA but based on the average of RSI values.

## 2. Detailed Breakdown of the Uptrick: RSI Histogram

### **2.1 Indicator Overview**

The Uptrick: RSI Histogram (USH) is a technical analysis tool that combines the RSI with a moving average to create a histogram that reflects momentum and trend strength.

**Key Components:**

- **RSI Calculation:** Determines the relative strength of price movements.

- **Moving Average Application:** Smooths the RSI values to provide a clearer trend indication.

- **Histogram Plotting:** Visualizes the deviation of the smoothed RSI from a neutral level.

### **2.2 Indicator Purpose**

The primary purpose of the USH is to provide a clear visual representation of the market's momentum and trend strength. It helps traders identify:

- **Bullish and Bearish Trends:** By showing how far the smoothed RSI is from the neutral 50 level.

- **Potential Reversal Points:** By highlighting changes in momentum.

### **2.3 Indicator Design**

**RSI Moving Average (RSI MA):** The RSI MA is a smoothed version of the RSI, calculated using a running moving average. This smooths out short-term fluctuations and provides a clearer indication of the underlying trend.

**Histogram Calculation:**

- **Neutral Level:** The histogram is plotted relative to the neutral level of 50. This level represents a balanced market where neither bulls nor bears have dominance.

- **Histogram Values:** The histogram bars show the difference between the RSI MA and the neutral level. Positive values indicate bullish momentum, while negative values indicate bearish momentum.

## 3. Calculation and Formula

### **3.1 RSI Calculation**

The RSI calculation involves:

1. **Average Gain and Loss:** Calculated over the specified length (e.g., 14 periods).

2. **Relative Strength (RS):** RS = Average Gain / Average Loss.

3. **RSI Formula:** RSI = 100 - (100 / (1 + RS)).

### **3.2 Moving Average Calculation**

For the USH indicator, the RSI is smoothed using a running moving average (RMA). The RMA formula is similar to that of the EMA but is based on averaging RSI values over the specified length.

### **3.3 Histogram Calculation**

The histogram value is calculated as:

- **Histogram Value = RSI MA - 50**

**Plotting the Histogram:**

- **Positive Histogram Values:** Indicate that the RSI MA is above the neutral level, suggesting bullish momentum.

- **Negative Histogram Values:** Indicate that the RSI MA is below the neutral level, suggesting bearish momentum.

## 4. Visual Representation

### **4.1 Histogram Bars**

The histogram is plotted as bars on the chart:

- **Bullish Bars:** Colored green when the RSI MA is above 50.

- **Bearish Bars:** Colored red when the RSI MA is below 50.

### **4.2 Customization Options**

Traders can customize:

- **RSI Length:** Adjust the length of the RSI calculation to match their trading style.

- **Bull and Bear Colors:** Choose colors for histogram bars to enhance visual clarity.

### **4.3 Interpretation**

**Bullish Signal:** A histogram bar that moves from red to green indicates a potential shift to a bullish trend.

**Bearish Signal:** A histogram bar that moves from green to red indicates a potential shift to a bearish trend.

## 5. Customization and User Settings

### **5.1 Adjusting RSI Length**

The length parameter determines the number of periods over which the RSI is calculated and smoothed. Shorter lengths make the RSI more sensitive to price changes, while longer lengths provide a smoother view of trends.

### **5.2 Color Settings**

Traders can adjust:

- **Bull Color:** Color of histogram bars indicating bullish momentum.

- **Bear Color:** Color of histogram bars indicating bearish momentum.

**Customization Benefits:**

- **Visual Clarity:** Traders can choose colors that stand out against their chart’s background.

- **Personal Preference:** Adjust settings to match individual trading styles and preferences.

## 6. Trading Strategies and Applications

### **6.1 Trend Following**

**Identifying Entry Points:**

- **Bullish Entry:** When the histogram changes from red to green, it signals a potential entry point for long positions.

- **Bearish Entry:** When the histogram changes from green to red, it signals a potential entry point for short positions.

**Trend Confirmation:** The histogram helps confirm the strength of a trend. Strong, consistent green bars indicate robust bullish momentum, while strong, consistent red bars indicate robust bearish momentum.

### **6.2 Swing Trading**

**Momentum Analysis:**

- **Entry Signals:** Look for significant shifts in the histogram to time entries. A shift from bearish to bullish (red to green) indicates potential for upward movement.

- **Exit Signals:** A shift from bullish to bearish (green to red) suggests a potential weakening of the trend, signaling an exit or reversal point.

### **6.3 Range Trading**

**Market Conditions:**

- **Consolidation:** The histogram close to zero suggests a range-bound market. Traders can use this information to identify support and resistance levels.

- **Breakout Potential:** A significant move away from the neutral level may indicate a potential breakout from the range.

### **6.4 Risk Management**

**Stop-Loss Placement:**

- **Bullish Positions:** Place stop-loss orders below recent support levels when the histogram is green.

- **Bearish Positions:** Place stop-loss orders above recent resistance levels when the histogram is red.

**Position Sizing:** Adjust position sizes based on the strength of the histogram signals. Strong trends (indicated by larger histogram bars) may warrant larger positions, while weaker signals suggest smaller positions.

## 7. Risk Management

### **7.1 Importance of Risk Management**

Effective risk management is crucial for long-term trading success. It involves protecting capital, managing losses, and optimizing trade setups.

### **7.2 Using USH for Risk Management**

**Stop-Loss and Take-Profit Levels:**

- **Stop-Loss Orders:** Use the histogram to set stop-loss levels based on trend strength. For instance, place stops below support levels in bullish trends and above resistance levels in bearish trends.

- **Take-Profit Targets:** Adjust take-profit levels based on histogram changes. For example, lock in profits as the histogram starts to shift from green to red.

**Position Sizing:**

- **Trend Strength:** Scale position sizes based on the strength of histogram signals. Larger histogram bars indicate stronger trends, which may justify larger positions.

- **Volatility:** Consider market volatility and adjust position sizes to mitigate risk.

## 8. Case Studies and Examples

### **8.1 Example 1: Bullish Trend**

**Scenario:** A trader notices a transition from red to green histogram bars.

**Analysis:**

- **Entry Point:** The transition indicates a potential bullish trend. The trader decides to enter a long position.

- **Stop-Loss:** Set stop-loss below recent support levels.

- **Take-Profit:** Consider taking profits as the histogram moves back towards zero or turns red.

**Outcome:** The bullish trend continues, and the histogram remains green, providing a profitable trade setup.

### **8.2 Example 2: Bearish Trend**

**Scenario:** A trader observes a transition from green to red histogram bars.

**Analysis:**

- **Entry Point:** The transition suggests a potential

bearish trend. The trader decides to enter a short position.

- **Stop-Loss:** Set stop-loss above recent resistance levels.

- **Take-Profit:** Consider taking profits as the histogram approaches zero or shifts to green.

**Outcome:** The bearish trend continues, and the histogram remains red, resulting in a successful trade.

## 9. Comparison with Other Indicators

### **9.1 RSI vs. USH**

**RSI:** Measures momentum and identifies overbought/oversold conditions.

**USH:** Builds on RSI by incorporating a moving average and histogram to provide a clearer view of trend strength and momentum.

### **9.2 RSI vs. MACD**

**MACD (Moving Average Convergence Divergence):** A trend-following momentum indicator that uses moving averages to identify changes in trend direction.

**Comparison:**

- **USH:** Provides a smoothed RSI perspective and visual histogram for trend strength.

- **MACD:** Offers signals based on the convergence and divergence of moving averages.

### **9.3 RSI vs. Stochastic Oscillator**

**Stochastic Oscillator:** Measures the level of the closing price relative to the high-low range over a specified period.

**Comparison:**

- **USH:** Focuses on smoothed RSI values and histogram representation.

- **Stochastic Oscillator:** Provides overbought/oversold signals and potential reversals based on price levels.

## 10. Advanced Usage and Tips

### **10.1 Combining Indicators**

**Multi-Indicator Strategies:** Combine the USH with other technical indicators (e.g., Moving Averages, Bollinger Bands) for a comprehensive trading strategy.

**Confirmation Signals:** Use the USH to confirm signals from other indicators. For instance, a bullish histogram combined with a moving average crossover may provide a stronger buy signal.

### **10.2 Customization Tips**

**Adjust RSI Length:** Experiment with different RSI lengths to match various market conditions and trading styles.

**Color Preferences:** Choose histogram colors that enhance visibility and align with personal preferences.

### **10.3 Continuous Learning**

**Backtesting:** Regularly backtest the USH with historical data to refine strategies and improve accuracy.

**Education:** Stay updated with trading education and adapt strategies based on market changes and personal experiences.

US M2### Relevance and Functionality of the "US M2" Indicator

#### Relevance

The "US M2" indicator is relevant for several reasons:

1. **Macro-Economic Insight**: The M2 money supply is a critical indicator of the amount of liquidity in the economy. Changes in M2 can significantly impact financial markets, including equities, commodities, and cryptocurrencies.

2. **Trend Identification**: By analyzing the M2 money supply with moving averages, the indicator helps identify long-term and short-term trends, providing insights into economic conditions and potential market movements.

3. **Trading Signals**: The indicator generates bullish and bearish signals based on moving average crossovers and the difference between current M2 values and their moving averages. These signals can be useful for making informed trading decisions.

#### How It Works

1. **Data Input**:

- **US M2 Money Supply**: The indicator fetches the US M2 money supply data using the "USM2" symbol with a monthly resolution.

2. **Moving Averages**:

- **50-Period SMA**: Calculates the Simple Moving Average (SMA) over 50 periods (months) to capture short-term trends.

- **200-Period SMA**: Calculates the SMA over 200 periods to identify long-term trends.

3. **Difference Calculation**:

- **USM2 Difference**: Computes the difference between the current M2 value and its 50-period SMA to highlight deviations from the short-term trend.

4. **Amplification**:

- **Amplified Difference**: Multiplies the difference by 100 to make the deviations more visible on the chart.

5. **Bullish and Bearish Conditions**:

- **Bullish Condition**: When the current M2 value is above the 50-period SMA, indicating a positive short-term trend.

- **Bearish Condition**: When the current M2 value is below the 50-period SMA, indicating a negative short-term trend.

6. **Short-Term SMA of Amplified Difference**:

- **14-Period SMA**: Applies a 14-period SMA to the amplified difference to smooth out short-term fluctuations and provide a clearer trend signal.

7. **Plots and Visualizations**:

- **USM2 Plot**: Plots the US M2 data for reference.

- **200-Period SMA Plot**: Plots the long-term SMA to show the broader trend.

- **Amplified Difference Histogram**: Plots the amplified difference as a histogram with green bars for bullish conditions and red bars for bearish conditions.

- **SMA of Amplified Difference**: Plots the 14-period SMA of the amplified difference to track the trend of deviations.

8. **Moving Average Cross Signals**:

- **Bullish Cross**: Plots an upward triangle when the 50-period SMA crosses above the 200-period SMA, signaling a potential long-term uptrend.

- **Bearish Cross**: Plots a downward triangle when the 50-period SMA crosses below the 200-period SMA, signaling a potential long-term downtrend.

### Summary

The "US M2" indicator provides a comprehensive view of the US M2 money supply, highlighting significant trends and deviations. By combining short-term and long-term moving averages with amplified difference analysis, it offers valuable insights and trading signals based on macroeconomic liquidity conditions.

Smart Money Analysis with Golden/Death Cross [YourTradingSensei]Description of the script "Smart Money Analysis with Golden/Death Cross":

This TradingView script is designed for market analysis based on the concept of "Smart Money" and includes the detection of Golden Cross and Death Cross signals.

Key features of the script:

Moving Averages (SMA):

Two moving averages are calculated: a short-term (50 periods) and a long-term (200 periods).

The intersections of these moving averages are used to determine Golden Cross and Death Cross signals.

High Volume:

The current trading volume is analyzed.

Periods of high volume are identified when the current volume exceeds the average volume by a specified multiplier.

Support and Resistance Levels:

Key support and resistance levels are determined based on the highest and lowest prices over a specified period.

Buy and Sell Signals:

Buy and sell signals are generated based on moving average crossovers, high volume, and the closing price relative to key levels.

Golden Cross and Death Cross:

A Golden Cross occurs when the short-term moving average crosses above the long-term moving average.

A Death Cross occurs when the short-term moving average crosses below the long-term moving average.

These signals are displayed on the chart with text color changes for better visualization.

Using the script:

The script helps traders visualize key signals and levels, aiding in making informed trading decisions based on the behavior of major market players and technical analysis.

Custom candle lighting(CCL) © 2024 by YourTradingSensei is licensed under CC BY-NC-SA 4.0. To view a copy of this license.

Coiled Moving AveragesThis indicator detects when 3 moving averages converge and become coiled. This indicates volatility contraction which often leads to volatility expansion, i.e. large price movements.

Moving averages are considered coiled when the percent difference from each moving average to the others is less than the Coil Tolerance % input value.

This indicator is unique in that it detects when moving averages converge within a specified percent range. This is in contrast to other indicators that only detect moving average crossovers, or the distance between price and a moving average.

This indicator includes options such as:

- % difference between the MAs to be considered coiled

- type and length of MAs

- background color to indicate when the MAs are coiled

- arrows to indicate if price is above or below the MAs when they become coiled

While coiling predicts an increased probability for volatility expansion, it does not necessarily predict the direction of expansion. However, the arrows which indicate whether price is above or below the moving average coil may increase the odds of a move in that direction. Bullish alignment of the moving averages (faster MAs above the slower MAs) may also increase the odds of a bullish break, while bearish alignment may increase the odds of a bearish break.

Note that mean reversion back to the MA coil is common after initial volatility expansion. This can present an entry opportunity for traders, as mean reversion may be followed by continuation in the direction of the initial break.

Experiment with different settings and timeframes to see how coiled MAs can help predict the onset of volatility.

Buy Only Strategy with Dynamic Re-Entry and ExitThe strategy aims to create a simple buy-only trading system based on moving average crossovers and the Weekly Commodity Channel Index (CCI) or Weekly Average Directional Index (ADX). It generates buy signals when the fast-moving average crosses above the slow-moving average and when the Weekly CCI and or Weekly ADX meet the specified conditions.

The strategy also allows for dynamic re-entry, which means it can open new long positions if the price goes above the three moving averages after an exit. However, the strategy will exit the long position if the price closes below the third moving average.

ENTRY CONDITIONS

The script defines the conditions for generating buy signals. It checks for two conditions for a valid buy signal:

• If the fast-moving average crosses above the slow-moving average -THERE IS Dynamic Re-Entry also

• If the user chooses HE OR SHE CAN FILTER TRADES BY USING CCI OR ADX

Dynamic Re-Entry:

the script allows for dynamic re-entry. If there is no active long position and the price is above all three moving averages a new long position is opened.

Exit Conditions

The script defines the exit condition for closing a long position. If the price closes below the third moving average, the script closes the long position.

IMPORTANT NOTICE

ONLY DAILY TIME FRAME

THERE WOULD BE WHIPSAW USE YOUR OWN ACCUMEN TO MINIMISE THEM

ITS ONLY BUY STRATEGY

EXIT CAN BE STRATEGY BASED OR SET PROFIT AND TARGETS AS PER RISK APETITE /RISK MANAGEMENT

DONT TRADE OPTIONS ON THIS

SUITABLE FOR STOCKS OF USA AND INDIAN MARKETS

ALWAYS REMEMBER TO DO YOUR OWN RESEARCH BEFORE TRADING AND INVESTING

Moving Average CandlesInspired by Ricardo Santos's " Multiple Moving Average Candle System V0" ()

This script plots 6 moving averages using the plotcandle function rather than the normal plot function. Result is a stylish indicator that shows moving average crossovers in a more visual way. Moving average type options available are , or Simple, Exponential, Hull, Relative, Volume Weighted, and Arnaud Legoux Moving Averages, Linear Regression Curve, and Median. Lengths for each can be set in settings along with selection specific parameters. Good for plotting/visualizing potential entry/exit points based on your preferred moving averages crossing over, or just as some eye candy.

RSI MA CrossBuilding onto the standard RSI indicator, with the following modification and improvements:

- Added signals for RSI moving average crossovers, which usually indicator a bull or bear trend

- Added option to use smoothed RSI line

- Added alert for crossover signals

Enjoy~~~!

Moving Average CombinationsThis moving average indicator is used to plot either EMA or SMA as per users choice. User also has the options to choose different type of sources for each of the moving average lines like high, low, close etc. Again, flexibility is added to plot moving averages of different timeframe than the current timeframe of the chart. By doing so in daily chart user can plot averages of different timeframe like hourly, weekly or monthly and vice versa. Length is also as per the choice of the user.

So for a example, in a daily timeframe chart you can plot 9SMA High Daily, 200EMA Close 1Hr, 200EMA Close 2Hr, 200EMA Close Daily, 9SMA High Weekly and so on. This will help in play moving average crossovers and contractions.

Label for each moving average line is also added.

trend_vol_forecastNote: The following description is copied from the script's comments. Since TradingView does not allow me to edit this description, please refer to the comments and release notes for the most up-to-date information.

-----------

USAGE

This script compares trend trading with a volatility stop to "buy and hold".

Trades are taken with the trend, except when price exceeds a volatility

forecast. The trend is defined by a moving average crossover. The forecast

is based on projecting future volatility from historical volatility.

The trend is defined by two parameters:

- long: the length of a long ("slow") moving average.

- short: the length of a short ("fast") moving average.

The trend is up when the short moving average is above the long. Otherwise

it is down.

The volatility stop is defined by three parameters:

- volatility window: determines the number of periods in the historical

volatility calculation. More periods means a slower (smoother)

estimate of historical volatility.

- stop forecast periods: the number of periods in the volatility

forecast. For example, "7" on a daily chart means that the volatility

will be forecasted with a one week lag.

- stop forecast stdev: the number of standard deviations in the stop

forecast. For example, "2" means two standard deviations.

EXAMPLE

The default parameters are:

- long: 50

- short: 20

- volatility window: 30

- stop forecast periods: 7

- stop forecast standard deviations: 1

The trend will be up when the 20 period moving average is above the 50

period moving average. On each bar, the historical volatility will be

calculated from the previous 30 bars. If the historical volatility is 0.65

(65%), then a forecast will be drawn as a fuchsia line, subtracting

0.65 * sqrt(7 / 365) from the closing price. If price at any point falls

below the forecast, the volatility stop is in place, and the trend is

negated.

OUTPUTS

Plots:

- The trend is shown by painting the slow moving average green (up), red

(down), or black (none; volatility stop).

- The fast moving average is shown in faint blue

- The previous volatility forecasts are shown in faint fuchsia

- The current volatility forecast is shown as a fuchsia line, projecting

into the future as far as it is valid.

Tables:

- The current historical volatility is given in the top right corner, as a

whole number percentage.

- The performance table shows the mean, standard deviation, and sharpe

ratio of the volatility stop trend strategy, as well as buy and hold.

If the trend is up, each period's return is added to the sample (the

strategy is long). If the trend is down, the inverse of each period's

return is added to the sample (the strategy is short). If there is no

trend (the volatility stop is active), the period's return is excluded

from the sample. Every period is added to the buy-and-hold strategy's

sample. The total number of periods in each sample is also shown.

Shapeshifting Moving Average - Switching From Low-Lag To SmoothThe term "shapeshifting" is more appropriate when used with something with a shape that isn't supposed to change, this is not the case of a moving average whose shape can be altered by the length setting or even by an external factor in the case of adaptive moving averages, but i'll stick with it since it describe the purpose of the proposed moving average pretty well.

In the case of moving averages based on convolution, their properties are fully described by the moving average kernel ( set of weights ), smooth moving averages tend to have a symmetrical bell shaped kernel, while low lag moving averages have negative weights. One of the few moving averages that would let the user alter the shape of its kernel is the Arnaud Legoux moving average, which convolve the input signal with a parametric gaussian function in which the center and width can be changed by the user, however this moving average is not a low-lagging one, as the weights don't include negative values.

Other moving averages where the user can change the kernel from user settings where already presented, i posted a lot of them, but they only focused on letting the user decrease or increase the lag of the moving average, and didn't included specific parameters controlling its smoothness. This is why the shapeshifting moving average is proposed, this parametric moving average will let the user switch from a smooth moving average to a low-lagging one while controlling the amount of lag of the moving average.

Settings/Kernel Interaction

Note that it could be possible to design a specific kernel function in order to provide a more efficient approach to today goal, but the original indicator was a simple low-lag moving average based on a modification of the second derivative of the arc tangent function and because i judged the indicator a bit boring i decided to include this parametric particularity.

As said the moving average "kernel", who refer to the set of weights used by the moving average, is based on a modification of the second derivative of the arc tangent function, the arc tangent function has a "S" shaped curve, "S" shaped functions are called sigmoid functions, the first derivative of a sigmoid function is bell shaped, which is extremely nice in order to design smooth moving averages, the second derivative of a sigmoid function produce a "sinusoid" like shape ( i don't have english words to describe such shape, let me know if you have an idea ) and is great to design bandpass filters.

We modify this 2nd derivative in order to have a decreasing function with negative values near the end, and we end up with:

The function is parametric, and the user can change it ( thus changing the properties of the moving average ) by using the settings, for example an higher power value would reduce the lag of the moving average while increasing overshoots. When power < 3 the moving average can act as a slow moving average in a moving average crossover system, as weights would not include negative values.

Here power = 0 and length = 50. The shapeshifting moving average can approximate a simple moving average with very low power values, as this would make the kernel approximate a rectangular function, however this is only a curiosity and not something you should do.

As A Smooth Moving Average

“So smooth, and so tranquil. It doesn't get any quieter than this”

A smooth moving average kernel should be : symmetrical, not to width and not to sharp, bell shaped curve are often appropriates, the proposed moving average kernel can be symmetrical and can return extremely smooth results. I will use the Blackman filter as comparison.

The smooth version of the moving average can be used when the "smooth" setting is selected. Here power can only be an even number, if power is odd, power will be equal to the nearest lowest even number. When power = 0, the kernel is simply a parabola:

More smoothness can be achieved by using power = 2

In red the shapeshifting moving average, in green a Blackman filter of both length = 100. Higher values of power will create lower negative values near the border of the kernel shape, this often allow to retain information about the peaks and valleys in the input signal. Power = 6 approximate the Blackman filter pretty well.

Conclusion

A moving average using a modification of the 2nd derivative of the arc tangent function as kernel has been presented, the kernel is parametric and allow the user to switch from a low-lag moving average where the lag can be increased/decreased to a really smooth moving average.

As you can see once you get familiar with a function shape, you can know what would be the characteristics of a moving average using it as kernel, this is where you start getting intimate with moving averages.

On a side note, have you noticed that the views counter in posted ideas/indicators has been removed ? This is truly a marvelous idea don't you think ?

Thanks for reading !

EMA inFusion Pro - Multiple SourcesEMA Fusion Pro: Dynamic Trend & Momentum Strategy with Three Exit Modes

EMA Fusion Pro is a highly customizable, multi-exit trend-following strategy designed for traders who value both precision and flexibility. By leveraging exponential moving averages (EMA), average directional index (ADX), and volume analysis, this strategy aims to capture trending market moves while offering three distinct exit modes for optimal risk management across varying market conditions.

Strategy Overview

This strategy systematically identifies potential entry points using a moving average crossover with highly configurable data sources (including price, volume, rate of change, or their Heikin Ashi versions) and filters signal quality with ADX trend strength and volume spikes. Each trade is managed with one of three advanced exit methodologies—reverse signal, ATR-based stop/take profit, or fixed percentage—giving you the control to adapt your risk profile to different market regimes.

Key Features

Customizable EMA Source: Calculate the core trend-filtering EMA from price (default), volume, rate of change, or their Heikin Ashi counterparts for unique market perspectives.

Trend Filter with ADX: Confirm entries only when the trend is strong, as measured by the user-adjustable ADX threshold.

Volume Spike Confirmation: Optional filter to only take trades with above-average volume activity, reducing false signals.

Three Exit Modes:

Reverse Signal: Exit trades when a new, opposite entry signal occurs.

ATR-Based Stop/Take Profit: Dynamic risk management using multiples of the average true range (ATR) for both take profit and stop loss.

Percent-Based Stop/Take Profit: Fixed-percentage risk management with user-defined thresholds.

Visual Annotations: Signal markers, EMA line color-coded by source, trend background coloring, and optional ATR/percent-based TP/SL levels.

Info Panel: Real-time display of all core indicators, current trading mode, exit parameters, and position status for quick oversight.

How It Works

Entry Logic: A crossover signal (above/below the EMA) triggers a new entry, but only if both ADX trend strength and (optionally) volume spike conditions are met.

Exit Logic: Three selectable modes allow you to exit trades on reverse signals, at a dynamic ATR-based profit or loss, or at a fixed percentage gain/loss.

Flexible Data Analysis: The EMA source can be chosen from six options—standard price, volume, rate of change, or their Heikin Ashi variants—allowing experimentation with different market dimensions.

Risk Management: All exits are precisely controlled, either by the next opposing signal, by volatility-adjusted levels, or by fixed risk/reward ratios.

Backtest & Optimization: The strategy is fully backtestable within TradingView’s Strategy Tester, with adjustable parameters for optimization.

Customization & Usage

Indicator Source: Select your preferred data type for EMA calculation, opening the door to creative strategy variations (e.g., volume momentum, pure price trend, rate of change divergence).

Filter Toggles: Enable/disable ADX and volume filters as desired—useful for different market environments.

Exit Mode Selection: Switch between reverse, ATR, or percent-based exits with a single parameter—ideal for adapting to ranging vs. trending markets.

Visual Clarity: The EMA line color reflects its underlying source, and the info panel summarizes all critical values for easy monitoring.

Who Should Use This Strategy?

Trend Followers seeking to ride strong moves with multiple exit options.

Experienced Traders who want to experiment with different data types (volume, momentum, Heikin Ashi) for trend analysis.

Algorithmic Traders looking for a robust, flexible base to build upon with their own ideas.

Getting Started

Apply the script to your chart and review default settings.

Customize parameters—EMA length, ADX threshold, volume settings, exit type—as desired.

Backtest on multiple instruments and timeframes to evaluate performance.

Optimize filters, exit rules, and risk parameters for your preferred trading style.

Monitor with the real-time info panel and trade alerts.

Disclaimer

This script is for educational and entertainment purposes only. It is not financial advice. Past performance is not indicative of future results. Always conduct thorough testing and consider your risk tolerance before trading real capital.

— Happy Trading —

Feel free to adapt, share, and contribute to this open-source strategy!

FUMO MA Cross Matrix 9/21/50/100/200 FUMO MA Cross Matrix is a flexible and advanced indicator designed for traders who rely on moving average crossovers as part of their strategy.

🔹 Key Features:

Supports 5 types of Moving Averages: EMA, SMA, SMMA (RMA), WMA, HMA.

Includes 5 standard MAs: 9, 21, 50, 100, 200 (toggle on/off individually).

Choose which MA crosses to monitor (9×21, 21×50, 50×100, 100×200, and 6 extended combinations).

On-chart signals (labels) when crosses occur.

Alerts system for every selected cross and also summary alerts (“Any Cross Up/Down”).

Option to trigger signals only on confirmed bars (no repaint).

Fully adjustable label visibility and signal style.

🔹 Use Cases:

Detect trend shifts (short-term vs long-term).

Build scalping, swing, or position trading strategies.

Combine with price action or volume analysis for stronger setups.

Quickly react to Golden Cross and Death Cross events.

🔹 How to Use:

Select your preferred MA type (EMA, SMA, etc.).

Enable the MAs (9, 21, 50, 100, 200) you want to plot.

Choose which crossovers to track in the settings.

Enable/disable on-chart labels for better visualization.

Set up alerts:

“CROSS UP/DOWN X>Y” for specific pairs.

“ANY CROSS UP/DOWN” for aggregated signals.

📌 Example Alerts

MA Cross UP 9>21 on BTCUSDT 15m @ 65432

Any selected MA cross DOWN on AAPL 1D @ 195.2

Simple Multi-Timeframe Trends with RSI (Realtime)Simple Multi-Timeframe Trends with RSI Realtime Updates

Overview

The Simple Multi-Timeframe Trends with RSI Realtime Updates indicator is a comprehensive dashboard designed to give you an at-a-glance understanding of market trends across nine key timeframes, from one minute (M1) to one month (M).

It moves beyond simple moving average crossovers by calculating a sophisticated Trend Score for each timeframe. This score is then intelligently combined into a single, weighted Confluence Signal , which adapts to your personal trading style. With integrated RSI and divergence detection, SMTT provides a powerful, all-in-one tool to confirm your trade ideas and stay on the right side of the market.

Key Features

Automatic Trading Presets: The most powerful feature of the script. Simply select your trading style, and the indicator will automatically adjust all internal parameters for you:

Intraday: Uses shorter moving averages and higher sensitivity, focusing on lower timeframe alignment for quick moves.

Swing Trading: A balanced preset using medium-term moving averages, ideal for capturing trends that last several days or weeks.

Investment: Uses long-term moving averages and lower sensitivity, prioritizing the major trends on high timeframes.

Advanced Trend Scoring: The trend for each timeframe isn't just "up" or "down". The score is calculated based on a combination of:

Price vs. Moving Average: Is the price above or below the MA?

MA Slope: Is the trend accelerating or decelerating? A steep slope indicates a strong trend.

Price Momentum: How quickly has the price moved recently?

Volatility Adjustment: The score's quality is adjusted based on current market volatility (using ATR) to filter out choppy conditions.

Weighted Confluence Score: The script synthesizes the trend scores from all nine timeframes into a single, actionable signal. The weights are dynamically adjusted based on your selected Trading Style , ensuring the most relevant timeframes have the most impact on the final result.

Integrated RSI & Divergence: Each timeframe includes a smoothed RSI value to help you spot overbought/oversold conditions. It also flags potential bullish (price lower, RSI higher) and bearish (price higher, RSI lower) divergences, which can be early warnings of a trend reversal.

Clean & Customizable Dashboard: The entire analysis is presented in a clean, easy-to-read table on your chart. You can choose its position and optionally display the raw numerical scores for a deeper analysis.

How to Use It

1. Add to Chart: Apply the "Simple Multi-Timeframe Trends" indicator to your chart.

2. Select Your Style: This is the most important step. Go to the indicator settings and choose the Trading Style that best fits your strategy (Intraday, Swing Trading, or Investment). All calculations will instantly adapt.

3. Analyze the Dashboard:

Look at the Trend row to see the direction and strength of the trend on individual timeframes. Strong alignment (e.g., all green or all red) indicates a powerful, market-wide move.

Check the RSI row. Is the trend overextended (RSI > 60) or is there room to run? Look for the fuchsia color, which signals a divergence and warrants caution.

Focus on the Signal row. This is your summary. A "STRONG SIGNAL" with high alignment suggests a high-probability setup. A "NEUTRAL" or "Weak" signal suggests waiting for a better opportunity.

4. Confirm Your Trades: Use the SMTT dashboard as a confirmation tool. For example, if you are looking for a long entry, wait for the dashboard to show a "BULLISH" or "STRONG SIGNAL" to confirm that the broader market structure supports your trade.

Dashboard Legend

Trend Row

This row shows the trend direction and strength for each timeframe.

⬆⬆ (Dark Green): Ultra Bullish - Very strong, established uptrend.

⬆ (Green): Strong Bullish - Confident uptrend.

▲ (Light Green): Bullish - The beginning of an uptrend or a weak uptrend.

━ (Orange): Neutral - Sideways or consolidating market.

▼ (Light Red): Bearish - The beginning of a downtrend or a weak downtrend.

⬇ (Red): Strong Bearish - Confident downtrend.

⬇⬇ (Dark Red): Ultra Bearish - Very strong, established downtrend.

RSI Row

This row displays the smoothed RSI value and its condition.

Green Text: Oversold (RSI < 40). Potential for a bounce or reversal upwards.

Red Text: Overbought (RSI > 60). Potential for a pullback or reversal downwards.

Fuchsia (Pink) Text: Divergence Detected! A potential reversal is forming.

White Text: Neutral (RSI between 40 and 60).

Signal Row

This is the final, weighted confluence of all timeframes.

Label:

🚀 STRONG SIGNAL / 💥 STRONG SIGNAL: High confluence and strong momentum.

🟢 BULLISH / 🔴 BEARISH: Clear directional bias across relevant timeframes.

🟡 Weak + / 🟠 Weak -: Minor directional bias, suggests caution.

⚪ NEUTRAL: No clear directional trend; market is likely choppy or undecided.

Numerical Score: The raw weighted confluence score. The further from zero, the stronger the signal.

Alignment %: The percentage of timeframes (out of 9) that are showing a clear bullish or bearish trend. Higher percentages indicate a more unified market.

Market Zone Analyzer[BullByte]Understanding the Market Zone Analyzer

---

1. Purpose of the Indicator

The Market Zone Analyzer is a Pine Script™ (version 6) indicator designed to streamline market analysis on TradingView. Rather than scanning multiple separate tools, it unifies four core dimensions—trend strength, momentum, price action, and market activity—into a single, consolidated view. By doing so, it helps traders:

• Save time by avoiding manual cross-referencing of disparate signals.

• Reduce decision-making errors that can arise from juggling multiple indicators.

• Gain a clear, reliable read on whether the market is in a bullish, bearish, or sideways phase, so they can more confidently decide to enter, exit, or hold a position.

---

2. Why a Trader Should Use It

• Unified View: Combines all essential market dimensions into one easy-to-read score and dashboard, eliminating the need to piece together signals manually.

• Adaptability: Automatically adjusts its internal weighting for trend, momentum, and price action based on current volatility. Whether markets are choppy or calm, the indicator remains relevant.

• Ease of Interpretation: Outputs a simple “BULLISH,” “BEARISH,” or “SIDEWAYS” label, supplemented by an intuitive on-chart dashboard and an oscillator plot that visually highlights market direction.

• Reliability Features: Built-in smoothing of the net score and hysteresis logic (requiring consecutive confirmations before flips) minimize false signals during noisy or range-bound phases.

---

3. Why These Specific Indicators?

This script relies on a curated set of well-established technical tools, each chosen for its particular strength in measuring one of the four core dimensions:

1. Trend Strength:

• ADX/DMI (Average Directional Index / Directional Movement Index): Measures how strong a trend is, and whether the +DI line is above the –DI line (bullish) or vice versa (bearish).

• Moving Average Slope (Fast MA vs. Slow MA): Compares a shorter-period SMA to a longer-period SMA; if the fast MA sits above the slow MA, it confirms an uptrend, and vice versa for a downtrend.

• Ichimoku Cloud Differential (Senkou A vs. Senkou B): Provides a forward-looking view of trend direction; Senkou A above Senkou B signals bullishness, and the opposite signals bearishness.

2. Momentum:

• Relative Strength Index (RSI): Identifies overbought (above its dynamically calculated upper bound) or oversold (below its lower bound) conditions; changes in RSI often precede price reversals.

• Stochastic %K: Highlights shifts in short-term momentum by comparing closing price to the recent high/low range; values above its upper band signal bullish momentum, below its lower band signal bearish momentum.

• MACD Histogram: Measures the difference between the MACD line and its signal line; a positive histogram indicates upward momentum, a negative histogram indicates downward momentum.

3. Price Action:

• Highest High / Lowest Low (HH/LL) Range: Over a defined lookback period, this captures breakout or breakdown levels. A closing price near the recent highs (with a positive MA slope) yields a bullish score, and near the lows (with a negative MA slope) yields a bearish score.

• Heikin-Ashi Doji Detection: Uses Heikin-Ashi candles to identify indecision or continuation patterns. A small Heikin-Ashi body (doji) relative to recent volatility is scored as neutral; a larger body in the direction of the MA slope is scored bullish or bearish.

• Candle Range Measurement: Compares each candle’s high-low range against its own dynamic band (average range ± standard deviation). Large candles aligning with the prevailing trend score bullish or bearish accordingly; unusually small candles can indicate exhaustion or consolidation.

4. Market Activity:

• Bollinger Bands Width (BBW): Measures the distance between BB upper and lower bands; wide bands indicate high volatility, narrow bands indicate low volatility.

• Average True Range (ATR): Quantifies average price movement (volatility). A sudden spike in ATR suggests a volatile environment, while a contraction suggests calm.

• Keltner Channels Width (KCW): Similar to BBW but uses ATR around an EMA. Provides a second layer of volatility context, confirming or contrasting BBW readings.

• Volume (with Moving Average): Compares current volume to its moving average ± standard deviation. High volume validates strong moves; low volume signals potential lack of conviction.

By combining these tools, the indicator captures trend direction, momentum strength, price-action nuances, and overall market energy, yielding a more balanced and comprehensive assessment than any single tool alone.

---

4. What Makes This Indicator Stand Out

• Multi-Dimensional Analysis: Rather than relying on a lone oscillator or moving average crossover, it simultaneously evaluates trend, momentum, price action, and activity.

• Dynamic Weighting: The relative importance of trend, momentum, and price action adjusts automatically based on real-time volatility (Market Activity State). For example, in highly volatile conditions, trend and momentum signals carry more weight; in calm markets, price action signals are prioritized.

• Stability Mechanisms:

• Smoothing: The net score is passed through a short moving average, filtering out noise, especially on lower timeframes.

• Hysteresis: Both Market Activity State and the final bullish/bearish/sideways zone require two consecutive confirmations before flipping, reducing whipsaw.

• Visual Interpretation: A fully customizable on-chart dashboard displays each sub-indicator’s value, regime, score, and comment, all color-coded. The oscillator plot changes color to reflect the current market zone (green for bullish, red for bearish, gray for sideways) and shows horizontal threshold lines at +2, 0, and –2.

---

5. Recommended Timeframes

• Short-Term (5 min, 15 min): Day traders and scalpers can benefit from rapid signals, but should enable smoothing (and possibly disable hysteresis) to reduce false whipsaws.

• Medium-Term (1 h, 4 h): Swing traders find a balance between responsiveness and reliability. Less smoothing is required here, and the default parameters (e.g., ADX length = 14, RSI length = 14) perform well.

• Long-Term (Daily, Weekly): Position traders tracking major trends can disable smoothing for immediate raw readings, since higher-timeframe noise is minimal. Adjust lookback lengths (e.g., increase adxLength, rsiLength) if desired for slower signals.

Tip: If you keep smoothing off, stick to timeframes of 1 h or higher to avoid excessive signal “chatter.”

---

6. How Scoring Works

A. Individual Indicator Scores

Each sub-indicator is assigned one of three discrete scores:

• +1 if it indicates a bullish condition (e.g., RSI above its dynamically calculated upper bound).

• 0 if it is neutral (e.g., RSI between upper and lower bounds).

• –1 if it indicates a bearish condition (e.g., RSI below its dynamically calculated lower bound).

Examples of individual score assignments:

• ADX/DMI:

• +1 if ADX ≥ adxThreshold and +DI > –DI (strong bullish trend)

• –1 if ADX ≥ adxThreshold and –DI > +DI (strong bearish trend)

• 0 if ADX < adxThreshold (trend strength below threshold)

• RSI:

• +1 if RSI > RSI_upperBound

• –1 if RSI < RSI_lowerBound

• 0 otherwise

• ATR (as part of Market Activity):

• +1 if ATR > (ATR_MA + stdev(ATR))

• –1 if ATR < (ATR_MA – stdev(ATR))

• 0 otherwise

Each of the four main categories shares this same +1/0/–1 logic across their sub-components.

B. Category Scores

Once each sub-indicator reports +1, 0, or –1, these are summed within their categories as follows:

• Trend Score = (ADX score) + (MA slope score) + (Ichimoku differential score)

• Momentum Score = (RSI score) + (Stochastic %K score) + (MACD histogram score)

• Price Action Score = (Highest-High/Lowest-Low score) + (Heikin-Ashi doji score) + (Candle range score)

• Market Activity Raw Score = (BBW score) + (ATR score) + (KC width score) + (Volume score)

Each category’s summed value can range between –3 and +3 (for Trend, Momentum, and Price Action), and between –4 and +4 for Market Activity raw.

C. Market Activity State and Dynamic Weight Adjustments

Rather than contributing directly to the netScore like the other three categories, Market Activity determines how much weight to assign to Trend, Momentum, and Price Action:

1. Compute Market Activity Raw Score by summing BBW, ATR, KCW, and Volume individual scores (each +1/0/–1).

2. Bucket into High, Medium, or Low Activity:

• High if raw Score ≥ 2 (volatile market).

• Low if raw Score ≤ –2 (calm market).

• Medium otherwise.

3. Apply Hysteresis (if enabled): The state only flips after two consecutive bars register the same high/low/medium label.

4. Set Category Weights:

• High Activity: Trend = 50 %, Momentum = 35 %, Price Action = 15 %.

• Low Activity: Trend = 25 %, Momentum = 20 %, Price Action = 55 %.

• Medium Activity: Use the trader’s base weight inputs (e.g., Trend = 40 %, Momentum = 30 %, Price Action = 30 % by default).

D. Calculating the Net Score

5. Normalize Base Weights (so that the sum of Trend + Momentum + Price Action always equals 100 %).

6. Determine Current Weights based on the Market Activity State (High/Medium/Low).

7. Compute Each Category’s Contribution: Multiply (categoryScore) × (currentWeight).

8. Sum Contributions to get the raw netScore (a floating-point value that can exceed ±3 when scores are strong).

9. Smooth the netScore over two bars (if smoothing is enabled) to reduce noise.

10. Apply Hysteresis to the Final Zone:

• If the smoothed netScore ≥ +2, the bar is classified as “Bullish.”

• If the smoothed netScore ≤ –2, the bar is classified as “Bearish.”

• Otherwise, it is “Sideways.”

• To prevent rapid flips, the script requires two consecutive bars in the new zone before officially changing the displayed zone (if hysteresis is on).

E. Thresholds for Zone Classification

• BULLISH: netScore ≥ +2

• BEARISH: netScore ≤ –2

• SIDEWAYS: –2 < netScore < +2

---

7. Role of Volatility (Market Activity State) in Scoring

Volatility acts as a dynamic switch that shifts which category carries the most influence:

1. High Activity (Volatile):

• Detected when at least two sub-scores out of BBW, ATR, KCW, and Volume equal +1.

• The script sets Trend weight = 50 % and Momentum weight = 35 %. Price Action weight is minimized at 15 %.

• Rationale: In volatile markets, strong trending moves and momentum surges dominate, so those signals are more reliable than nuanced candle patterns.

2. Low Activity (Calm):

• Detected when at least two sub-scores out of BBW, ATR, KCW, and Volume equal –1.

• The script sets Price Action weight = 55 %, Trend = 25 %, and Momentum = 20 %.

• Rationale: In quiet, sideways markets, subtle price-action signals (breakouts, doji patterns, small-range candles) are often the best early indicators of a new move.

3. Medium Activity (Balanced):

• Raw Score between –1 and +1 from the four volatility metrics.

• Uses whatever base weights the trader has specified (e.g., Trend = 40 %, Momentum = 30 %, Price Action = 30 %).

Because volatility can fluctuate rapidly, the script employs hysteresis on Market Activity State: a new High or Low state must occur on two consecutive bars before weights actually shift. This avoids constant back-and-forth weight changes and provides more stability.

---

8. Scoring Example (Hypothetical Scenario)

• Symbol: Bitcoin on a 1-hour chart.

• Market Activity: Raw volatility sub-scores show BBW (+1), ATR (+1), KCW (0), Volume (+1) → Total raw Score = +3 → High Activity.

• Weights Selected: Trend = 50 %, Momentum = 35 %, Price Action = 15 %.

• Trend Signals:

• ADX strong and +DI > –DI → +1

• Fast MA above Slow MA → +1

• Ichimoku Senkou A > Senkou B → +1

→ Trend Score = +3

• Momentum Signals:

• RSI above upper bound → +1

• MACD histogram positive → +1

• Stochastic %K within neutral zone → 0

→ Momentum Score = +2

• Price Action Signals:

• Highest High/Lowest Low check yields 0 (close not near extremes)

• Heikin-Ashi doji reading is neutral → 0

• Candle range slightly above upper bound but trend is strong, so → +1

→ Price Action Score = +1

• Compute Net Score (before smoothing):

• Trend contribution = 3 × 0.50 = 1.50

• Momentum contribution = 2 × 0.35 = 0.70

• Price Action contribution = 1 × 0.15 = 0.15

• Raw netScore = 1.50 + 0.70 + 0.15 = 2.35

• Since 2.35 ≥ +2 and hysteresis is met, the final zone is “Bullish.”

Although the netScore lands at 2.35 (Bullish), smoothing might bring it slightly below 2.00 on the first bar (e.g., 1.90), in which case the script would wait for a second consecutive reading above +2 before officially classifying the zone as Bullish (if hysteresis is enabled).

---

9. Correlation Between Categories

The four categories—Trend Strength, Momentum, Price Action, and Market Activity—often reinforce or offset one another. The script takes advantage of these natural correlations:

• Bullish Alignment: If ADX is strong and pointed upward, fast MA is above slow MA, and Ichimoku is positive, that usually coincides with RSI climbing above its upper bound and the MACD histogram turning positive. In such cases, both Trend and Momentum categories generate +1 or +2. Because the Market Activity State is likely High (given the accompanying volatility), Trend and Momentum weights are at their peak, so the netScore quickly crosses into Bullish territory.

• Sideways/Consolidation: During a low-volatility, sideways phase, ADX may fall below its threshold, MAs may flatten, and RSI might hover in the neutral band. However, subtle price-action signals (like a small breakout candle or a Heikin-Ashi candle with a slight bias) can still produce a +1 in the Price Action category. If Market Activity is Low, Price Action’s weight (55 %) can carry enough influence—even if Trend and Momentum are neutral—to push the netScore out of “Sideways” into a mild bullish or bearish bias.

• Opposing Signals: When Trend is bullish but Momentum turns negative (for example, price continues up but RSI rolls over), the two scores can partially cancel. Market Activity may remain Medium, in which case the netScore lingers near zero (Sideways). The trader can then wait for either a clearer momentum shift or a fresh price-action breakout before committing.

By dynamically recognizing these correlations and adjusting weights, the indicator ensures that:

• When Trend and Momentum align (and volatility supports it), the netScore leaps strongly into Bullish or Bearish.

• When Trend is neutral but Price Action shows an early move in a low-volatility environment, Price Action’s extra weight in the Low Activity State can still produce actionable signals.

---

10. Market Activity State & Its Role (Detailed)

The Market Activity State is not a direct category score—it is an overarching context setter for how heavily to trust Trend, Momentum, or Price Action. Here’s how it is derived and applied:

1. Calculate Four Volatility Sub-Scores:

• BBW: Compare the current band width to its own moving average ± standard deviation. If BBW > (BBW_MA + stdev), assign +1 (high volatility); if BBW < (BBW_MA × 0.5), assign –1 (low volatility); else 0.

• ATR: Compare ATR to its moving average ± standard deviation. A spike above the upper threshold is +1; a contraction below the lower threshold is –1; otherwise 0.

• KCW: Same logic as ATR but around the KCW mean.

• Volume: Compare current volume to its volume MA ± standard deviation. Above the upper threshold is +1; below the lower threshold is –1; else 0.

2. Sum Sub-Scores → Raw Market Activity Score: Range between –4 and +4.

3. Assign Market Activity State:

• High Activity: Raw Score ≥ +2 (at least two volatility metrics are strongly spiking).

• Low Activity: Raw Score ≤ –2 (at least two metrics signal unusually low volatility or thin volume).

• Medium Activity: Raw Score is between –1 and +1 inclusive.

4. Hysteresis for Stability:

• If hysteresis is enabled, a new state only takes hold after two consecutive bars confirm the same High, Medium, or Low label.

• This prevents the Market Activity State from bouncing around when volatility is on the fence.

5. Set Category Weights Based on Activity State:

• High Activity: Trend = 50 %, Momentum = 35 %, Price Action = 15 %.

• Low Activity: Trend = 25 %, Momentum = 20 %, Price Action = 55 %.

• Medium Activity: Use trader’s base weights (e.g., Trend = 40 %, Momentum = 30 %, Price Action = 30 %).

6. Impact on netScore: Because category scores (–3 to +3) multiply by these weights, High Activity amplifies the effect of strong Trend and Momentum scores; Low Activity amplifies the effect of Price Action.

7. Market Context Tooltip: The dashboard includes a tooltip summarizing the current state—e.g., “High activity, trend and momentum prioritized,” “Low activity, price action prioritized,” or “Balanced market, all categories considered.”

---

11. Category Weights: Base vs. Dynamic

Traders begin by specifying base weights for Trend Strength, Momentum, and Price Action that sum to 100 %. These apply only when volatility is in the Medium band. Once volatility shifts:

• High Volatility Overrides:

• Trend jumps from its base (e.g., 40 %) to 50 %.

• Momentum jumps from its base (e.g., 30 %) to 35 %.

• Price Action is reduced to 15 %.

Example: If base weights were Trend = 40 %, Momentum = 30 %, Price Action = 30 %, then in High Activity they become 50/35/15. A Trend score of +3 now contributes 3 × 0.50 = +1.50 to netScore; a Momentum +2 contributes 2 × 0.35 = +0.70. In total, Trend + Momentum can easily push netScore above the +2 threshold on its own.

• Low Volatility Overrides:

• Price Action leaps from its base (30 %) to 55 %.

• Trend falls to 25 %, Momentum falls to 20 %.

Why? When markets are quiet, subtle candle breakouts, doji patterns, and small-range expansions tend to foreshadow the next swing more effectively than raw trend readings. A Price Action score of +3 in this state contributes 3 × 0.55 = +1.65, which can carry the netScore toward +2—even if Trend and Momentum are neutral or only mildly positive.

Because these weight shifts happen only after two consecutive bars confirm a High or Low state (if hysteresis is on), the indicator avoids constantly flipping its emphasis during borderline volatility phases.

---

12. Dominant Category Explained

Within the dashboard, a label such as “Trend Dominant,” “Momentum Dominant,” or “Price Action Dominant” appears when one category’s absolute weighted contribution to netScore is the largest. Concretely:

• Compute each category’s weighted contribution = (raw category score) × (current weight).

• Compare the absolute values of those three contributions.

• The category with the highest absolute value is flagged as Dominant for that bar.

Why It Matters:

• Momentum Dominant: Indicates that the combined force of RSI, Stochastic, and MACD (after weighting) is pushing netScore farther than either Trend or Price Action. In practice, it means that short-term sentiment and speed of change are the primary drivers right now, so traders should watch for continued momentum signals before committing to a trade.

• Trend Dominant: Means ADX, MA slope, and Ichimoku (once weighted) outweigh the other categories. This suggests a strong directional move is in place; trend-following entries or confirming pullbacks are likely to succeed.

• Price Action Dominant: Occurs when breakout/breakdown patterns, Heikin-Ashi candle readings, and range expansions (after weighting) are the most influential. This often happens in calmer markets, where subtle shifts in candle structure can foreshadow bigger moves.

By explicitly calling out which category is carrying the most weight at any moment, the dashboard gives traders immediate insight into why the netScore is tilting toward bullish, bearish, or sideways.

---